Disclaimer: The Lemon Pros do not offer assistance with car repossession; this blog is for information purposes only.

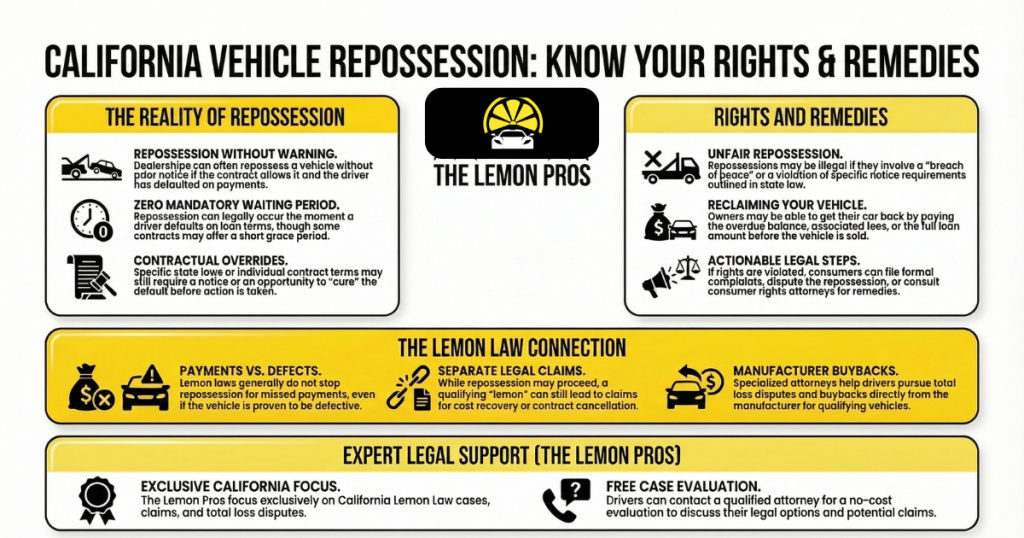

Yes, a dealership can repossess your vehicle if you default on your loan, such as by missing payments or violating the terms of the contract. In most states, they may do this without prior notice, as long as the repossession is carried out lawfully. However, they cannot use force, threats, or cause a disturbance during the process, as this would be considered a breach of the peace. If a breach of the peace occurs, you may have legal grounds to challenge the repossession or seek damages.

The Lemon Pros are experts in dealing with the Lemon Law and defective vehicles. Since our practice area is focused on lemon vehicles, we have been able to secure compensation for drivers. Contact us today to get a free consultation about your branded title vehicle!

This guide explains California repossession laws, your rights, how your property is protected, and what you can do to avoid having your vehicle repossessed.

What Does It Mean When a Dealership Repossesses Your Car?

When a dealership repossesses your car, the creditor takes back the vehicle because the borrower has defaulted on the financing agreement tied to the debt. In many states, a lender can repossess a vehicle as soon as the borrower defaults on the loan or lease.

Your contract likely contains a self-help clause allowing the lender to repossess the car without going to court, and in many states, the lender is not required to notify you before taking the car. Default may occur due to missed payments, failing to maintain required insurance coverage, or other breach of contract issues, such as using the vehicle for illegal activities or violating usage terms.

There are still legal restrictions on repossession. When taking the car, the lender cannot violate the peace by using force, threats, or unauthorized entry. If payments are not made on time, some lenders may also use kill switches to keep a car from starting, which could be considered a form of repossession.

The majority of states mandate that lenders notify borrowers prior to the sale of a repossessed vehicle. After the vehicle is taken, the creditor usually sells it in a commercially reasonable manner to recover the remaining debt.

There are two types of repossession: voluntary and involuntary. Voluntary repossession occurs when a borrower returns the vehicle to the creditor, which may reduce repossession costs but does not eliminate the remaining debt after the sale. Involuntary repossession happens when the lender takes the vehicle without the borrower’s consent, often after missed payments and sometimes without prior notice.

If a borrower has paid at least 30% of their loan, they may receive a notice of redemption allowing them to recover the vehicle, and they may be able to buy it back by paying the past-due balance and repossession costs. If you believe your vehicle was wrongfully repossessed, you may file a complaint or seek legal advice.

Dealership Repossession vs. Bank Repossession

Not all vehicle repossessions follow the same process. Whether your car is financed through a dealership or a traditional lender like a bank, the rules, timelines, and consumer protections can differ significantly. Understanding these key differences can help you know what to expect, protect your rights, and take the right steps if you fall behind on payments.

| Category | Dealership Repossession | Bank Repossession |

|---|---|---|

| Party Initiating Repossession | The car dealership (often in buy here, pay here financing arrangements) | A bank, credit union, or third-party auto lender |

| Typical Timelines | Usually faster; it can occur shortly after missed payments due to direct control over financing. | May take longer; lenders often allow multiple missed payments before action. |

| Consumer Notification Requirements | May provide limited notice depending on contract terms and state laws | Typically requires formal notices, including default and right-to-cure notices |

| Legal Rights | Governed by contract terms and state repossession laws, with fewer structured protections in some cases | More regulated; subject to federal and state lending laws with clearer borrower protections |

| Redemption Options | May allow reinstatement or payoff, but terms are often stricter and less flexible. | Usually offers reinstatement or redemption rights, sometimes with structured payment plans. |

Borrowers may be caught off guard by dealership repossessions, which typically occur more quickly and with fewer procedural protections. On the other hand, bank repossessions might take longer, but they frequently entail better communication and more organized chances to settle the default before losing the car.

Legal Rights of Dealerships vs. Consumers in Vehicle Repossession

Vehicle repossession is governed by both federal and state laws that balance the rights of lenders with protections for consumers. Under U.S. law, lenders or dealerships can repossess a vehicle when a borrower defaults on the loan. However, repossession must occur without breaching the peace, meaning the lender cannot use force, threats, or illegal entry during the process.

According to the repossession-than-pre-pandemic Consumer Financial Protection Bureau (CFPB), in December 2022, approximately 0.75% of all outstanding auto loans were assigned to repossession, representing a 22.5% increase from December 2019, when the rate was 0.61%. Dealerships and lenders generally rely on the loan contract to determine when repossession is allowed. These agreements typically include default clauses that outline what constitutes a breach.

Once a default occurs, the dealership or lender may have the legal right to repossess the vehicle and may also be required to provide notice about the repossession and any upcoming sale of the vehicle. Consumers also have important protections, particularly under state laws.

In California, repossession rules include requirements for post-repossession notices, the right to reinstate a loan in some situations, and disclosures about personal property left in the vehicle. These regulations help ensure that borrowers are informed of their rights and have an opportunity to address the default before or after the repossession process continues.

“As a general rule, repossession laws are designed to balance the lender’s right to recover collateral with the consumer’s right to fair treatment,” explains Arash Khorsandi, Attorney, The Lemon Pros. “The biggest legal issue we see is not the repossession itself, but how it is carried out, particularly when it involves a breach of the peace or improper notice.”

While repossession can feel sudden and unfair, lenders also take on financial risk when issuing auto loans. Repossession is often a last resort used to recover losses, especially when borrowers stop communicating or fail to make arrangements. That said, the law still requires lenders to follow strict rules, and consumers have the right to challenge any violations.

Can a Dealership Repo your Car?

When you purchase a vehicle, the dealership must find a lender to finance the agreement. The dealership generally includes a ten-day period in the agreement, but it can be longer. If you are current on your payments and the dealership cannot find a lender after that window, they cannot legally repossess your vehicle for that reason. The dealership will be required to step into the role of the lender and finance the agreement.

However, dealerships are generally allowed to legally repossess your vehicle if you miss a payment, regardless of whether it is by a day or two. A repossessed vehicle is only a valid solution if you have defaulted on the loan agreement. Nevertheless, if you stop making your payments because the dealership fails to provide you with registration within three months, the dealership cannot repossess your vehicle.

When Can the Dealership Repo Your Car?

A repossession agent will usually get involved if you are late on your payments or if you default. Even if you are a few days late on your car payments, the dealership has the right to repossess your car. Under California law, the dealership can also start the car repossession process if the sales contract is breached.

For these reasons, you must understand your agreement with the finance company. You wouldn’t want to violate any of the terms with the car loan lender, which could lead to possible repossession.

What Is the Legal Process for Repossession in California?

The repossession agency and guidelines are all governed by federal and state laws, including the Uniform Commercial Code (UCC) and the federal Consumer Financial Protection Bureau (CFPB). For the repo company to take action, the following steps must occur.

Default on Loan Payments

The first step under California repossession laws happens when consumers stop paying the auto loans. Missed payments are considered a breach of contract, giving rights to the financial institution to take your car. It doesn't matter if you are one day or 60 days late; once you've missed the payment, you've opened the door to repossession.

Written Notice

Under California’s repossession laws, the repo agent must provide a notice indicating what can be done to avoid having a repossessed car and when the deadline is. In some cases, there may still be a way to work with the loan company to get back into good standing. By paying the remaining balance, you may be able to get current and hold off the repossession agents.

Repossession of Your Personal Property

If the deadline comes with no resolution, the repossession agencies have the right to take your car. The car can be given back as a voluntary surrender (known as voluntary repossession), or it can be taken. However, repossession agencies may not breach the peace to do so. While the car is usually taken from a publicly accessible place, such as a parking lot, it can be removed from private property. However, no force can be used, and the repo agents are not permitted to trespass or violate any laws.

Notice of Sale

Repossessed vehicles are going to be sold, but you are to receive notice of this action before it occurs. If the vehicle is sold at a dealer-only auction, you won't be able to attend and buy back the vehicle. You would need to check with the auction house's rules before attending.

Repossessed Vehicle Sold

To receive the remainder of the portion of the loan balance, California repossession law allows for the vehicle to be sold through a private sale or public auction. After the lender sells, the money goes toward paying down the loan, but it may not fulfill it completely. If the entire loan isn’t paid off, the dealership may file legal action to hold you responsible for the balance and any costs related to the repossession. You may receive a court order and be slapped with a deficiency judgment for breaching the original contract.

The California Department of Consumer Affairs (DCA) has a regulatory role in overseeing consumer-related concerns, including concerns of vehicle repossession. Even though the DCA itself doesn’t handle repossession cases, it will provide information, assistance, and resources to consumers who face repossession or have questions regarding their rights.

What Should You Do If You Fall Behind on Car Payments?

The car loan terms set forth what you are expected to pay and how often. As part of the loan agreement, you’ve acknowledged that if you don’t pay, legal action can be taken. Not only may the car be repossessed, but the default could negatively affect your score on your credit report.

If you are behind on your payments, you should communicate with the lender or dealership before repossession occurs. They will often work with you to find a way to keep your vehicle by reducing your payment, lowering the interest rate, or waiving a payment by adding it to the back end of the contract.

Most lenders do not want to repossess the vehicle or take it to auction. They will not receive fair market value at the auction, meaning it will be sold for far less than its worth. That leaves them with the hassle of fighting you for the rest of the money, which can be a long and drawn-out process. For this reason, the loan company would rather you catch up on what's owed and start making timely payments in the future.

What Happens After Vehicle Repossession?

If your vehicle is legally repossessed, the lender will try to sell it at an auction as soon as possible to satisfy the outstanding loan. This may be problematic to you because the vehicle could sell for less than what you still owe on it, with most repossessed vehicles bringing in far less than the typical resale price. If that happens, you will still be liable to pay that difference in addition to having a repossession on your credit history.

However, not all dealerships and lenders follow the laws of repossession in California. Therefore, their actions may spark one of the many reasons to sue a dealership, leaving you with the ability to get compensation.

If you believe that the dealership illegally repossessed your vehicle, we can assist you in recovering your money or personal property. At times, we can force the dealership or lender to pay you extra corrective compensation. Make sure you keep records of any communication or notifications from the dealership or the lender, which can help prove that the lender didn't provide notice of the upcoming repossession or violated the terms.

First, you must receive prior notice from the lender or repossession companies with clear deadlines. Once the car is repossessed, the agency must store the vehicle properly and provide you with adequate notification about the upcoming sale. You have the opportunity to reclaim the vehicle and your personal property if you can get current on the late payments and other fees that are owed.

If you are unable to meet these obligations, the vehicle is sold, and the money earned goes toward the deficiency balance. If the entire amount isn’t covered, you are still liable for the remainder and any other late fees or expenses that have been added.

Our 3-Step Plan to Handle Repossession Risk

Taking the appropriate action early on, before late payments become a major issue, is the first step in preventing repossession. This straightforward three-step strategy explains how to safeguard your car, comprehend the conditions of your loan, and cooperate with your lender to maintain good standing. You can frequently avoid repossession or lessen its financial impact by taking prompt, calculated action.

- Step 1: Review Your Contract ImmediatelyCheck for default terms, grace periods, and any clauses about repossession or notice requirements.

- Step 2: Communicate EarlyIn our experience, lenders are far more willing to offer solutions before the account becomes severely delinquent.

- Step 3: Take Action Before Default EscalatesOptions like refinancing, payment restructuring, or voluntary surrender can significantly reduce long-term financial damage.

Case Example: Wrongful Repossession in California

In one instance we looked at, a California driver's car was repossessed two days after they failed to make a payment, even though their contract had a brief grace period. Concerns about a breach of the peace were raised when the borrower objected to the repossession agent's attempt to remove the vehicle from a gated driveway.

Following an examination of the circumstances, the borrower contested the repossession and was successful in obtaining compensation because of incorrect procedures. This kind of situation emphasizes how important it is to comprehend the terms of your contract and your legal rights both before and after a repossession.

What Are the Best Resources and Legal Help for Car Repossession Agents?

If you are facing vehicle repossession, there are ways to get help. For starters, we recommend reading the repossession guidelines set forth by the repossessions-california-registered-vehicles California Department of Motor Vehicles. We also suggest talking with your car insurance company about pausing or suspending coverage while you don’t have the vehicle in your possession. Find out what this car insurance lapse means for you, especially as you move forward to make a future car deal.

When facing repossession, the repo agent must be registered with the Bureau of Security and Investigative Services. Only a licensed agent is permitted to repossess your car. As they search for the vehicle, they may figure out how to get around a locked garage, private building, or gated community where the car is being kept. However, they must retain lawful control of their actions. Yes, they can take the car from a publicly accessible place, but no physical force may be used, and laws cannot be broken when they repossess your car.

As the legal owner of the private property, you may have rights concerning how the car is repossessed. For this reason, it’s best to contact a qualified attorney if you are worried about your rights being violated.

What Can You Do to Avoid Dealership Repossession?

Avoiding dealership repossession often starts with staying current on your loan payments and addressing financial issues early. If you anticipate missing a payment, contact the dealership or lender as soon as possible. Many lenders are willing to discuss temporary solutions, such as adjusted payment dates or short-term payment arrangements, especially when borrowers communicate before the account falls seriously behind.

It is also important to review your loan agreement carefully. Financing contracts typically include default clauses that explain what happens if payments are missed or other terms are violated. Understanding these terms helps you know your obligations and may prevent accidental breaches, such as failing to maintain required insurance coverage.

If keeping up with payments becomes difficult, several options may help you avoid repossession. Refinancing the loan, negotiating a payment plan, or even choosing voluntary surrender can sometimes reduce financial consequences compared to forced repossession. In situations where repossession relates to ongoing vehicle defects, consumer protections like lemon laws may also apply, giving buyers potential legal options if the vehicle repeatedly fails despite repair attempts.

Need Help With a Dealership Dispute?

Before dealing with any repo company, it’s best to have a team of legal professionals on your side, watching out for your rights. This guide stands out for its emphasis on real-world situations, useful preventative techniques, and concise explanations of your legal rights. This ensures that you are not only informed but also ready to act in the event that repossession becomes a possibility.

For excellent counsel, you want a qualified attorney-cost lemon law attorney such as The Lemon Pros. Our team of Lemon Law attorneys in California focuses exclusively on California Lemon Law cases and has helped drivers pursue claims, total loss disputes, and manufacturer buybacks. Contact us today for a free case evaluation to discuss your options at no cost.

Frequently Asked Questions

Have questions about your car problems? Here are answers to some of the most common car problems we encountered relating to lemon law.

Can a Dealership Repossess My Car Without Warning?

Yes, in many cases, a dealership can repossess your car without prior warning if your contract allows it and you’ve defaulted on payments. However, some state laws or contract terms may still require notice or an opportunity to cure the default.

What Can I Do if My Car Was Repossessed Unfairly?

You can review your contract and state laws to determine if the repossession violated your rights, such as a lack of proper notice or breach of peace. If violations occurred, you may file a complaint, dispute the action, or consult a consumer rights attorney for possible legal remedies.

Does the Lemon Law Protect Me From Repossession?

Lemon laws generally do not stop repossession if you fall behind on payments, even if the vehicle has defects. However, if your car qualifies as a lemon, you may have separate legal claims that could help you recover costs or cancel the contract.

How Long Does a Dealership Have to Wait Before Repossessing?

There is usually no mandatory waiting period, and repossession can occur as soon as you default on the loan terms. That said, some lenders or contracts may allow a short grace period before taking action.

Can I Get My Car Back After Repossession?

Yes, you may be able to reclaim your car by paying the overdue balance, fees, or the full loan amount, depending on the agreement. Acting quickly is important, as the vehicle may be sold if you do not exercise your redemption rights within the allowed timeframe.

Arash Khorsandi, Esq.

Founding PartnerArash Khorsandi, Esq. is the co-founder of The Lemon Pros. A fierce California Lemon Law attorney since age 24, he has built an all-star team and recovered millions in settlements for California consumers.

View Attorney Profile →